Regardless of preliminary considerations that tariffs would push mortgage charges as much as 8% and scale back housing demand, this week has introduced some encouraging information. The ten-year yield has remained secure at a vital technical degree and even reversed course, leading to improved mortgage charges. Moreover, housing demand has surprisingly held up, even with elevated mortgage charges.

Whereas the rise in demand might not be important, it’s nonetheless a optimistic improvement, and that’s price celebrating! Let’s check out the newest housing knowledge to realize insights into the market as we strategy the tip of the yr.

10-year yield and mortgage charges

My 2024 forecast included:

A variety for mortgage charges between 7.25%-5.75%

A variety for the 10-year yield between 4.25%-3.21%

The latest lower in mortgage charges may be attributed to dynamics within the bond market and the present sentiment amongst bond merchants. They see potential beneficial properties by buying the 10-year bond at its present degree, particularly now that the Citigroup Financial Shock Index has peaked within the quick time period and has pale.

Beforehand, there was important concern about the potential for a brand new wave of inflation, which might require elevating rates of interest, which I threw chilly water on in a latest HousingWire Each day podcast. Nevertheless, the latest peak within the 10-year yield was round 5% in 2023, and the downtrend from that degree is undamaged for now. So, so long as financial knowledge doesn’t shock the upside, bond yields ought to keep distant from 5%, which suggests mortgage charges gained’t get shut to eight%.

Once I discuss a Santa Clause rally, I imply folks shopping for the 10-year yield and driving mortgage charges decrease, because of the sluggish dance between the 10-year yield and mortgage charges. That is what occurred within the final two years. We’ll see if we get a repeat this yr.

Mortgage spreads

The mortgage unfold state of affairs has improved in 2024, particularly in comparison with the powerful instances in 2023. Due to this optimistic change, mortgage charges reached 6% with out the 10-year yield reaching 3.37% in 2024. Simply think about if spreads hadn’t improved — mortgage charges might be over 7.50% proper now!

Whereas we’ve seen a slight improve in spreads since mortgage charges began rising in September, it’s necessary to notice that they’re nonetheless in a a lot better place than the height ranges we skilled final yr. If spreads had remained as excessive as in 2023, mortgage charges immediately can be about 0.60% greater. On the flip facet, if we have been taking a look at common spreads, we’d see mortgage charges dropping by round 0.93% to 1.03%. Total, it’s encouraging to see progress within the mortgage market!

Weekly pending gross sales

The weekly pending contract knowledge from Altos Analysis provides us a unprecedented glimpse into real-time housing demand. It’s attention-grabbing to see how this knowledge follows seasonal developments, as proven within the chart under. At first, we noticed some strong efficiency when mortgage charges have been shut to six%. It’s encouraging to see pending contracts holding up yr over yr, although residence costs and mortgage charges have been greater lately. This development has piqued my curiosity, and I’m excited to control it! Think about if mortgage charges simply stayed in a spread between 5.75%-6.25% for 12 months.

That is the weekly pending gross sales for final week over the last few years:

2024: 317,0802023: 296,6152022: 299,312

Whereas our pending contract knowledge confirmed year-over-year development months in the past, the NAR’s pending residence gross sales have solely now caught up.

Buy utility knowledge

The latest buy utility knowledge was fairly shocking. Each time mortgage charges rise from a decrease development, the consequences are hostile for a while. Nevertheless, final week’s buy apps knowledge confirmed 12% week-to-week development, which now makes a optimistic development for the earlier seven weeks, which was not in my bingo card for the vacations. The final seven weeks:

When mortgage charges have been operating greater earlier within the yr (between 6.75%-7.50%), that is what the acquisition utility knowledge appeared like:

14 adverse prints

2 flat prints

2 optimistic prints

When mortgage charges began falling in mid-June, right here’s what buy purposes appeared like:

12 optimistic prints

5 adverse prints

1 flat print

With two years of knowledge, we observe a optimistic development development in buy purposes when mortgage charges strategy 6%.

Weekly housing stock knowledge

Housing stock fell final week, which is typical at the moment of yr. We must always anticipate a decline in stock till the spring season begins heating up once more. The height in 2024 stock will likely be 739,434, which isn’t a standard degree for stock, however a minimum of we’ve seen good, wholesome development this yr. The year-over-year stock development is the perfect housing story for 2024.

Weekly stock change (Nov. 22-Nov. 29): Stock fell from 719,055 to 706,554

The identical week final yr (Nov. 24-Nov. 30): Stock fell from 565,875 to 555,717

The all-time stock backside was in 2022 at 240,497

The stock peak for 2024 to this point is 739,434

For some context, energetic listings for this week in 2015 have been 1,082,020

At the moment, new listings knowledge is experiencing a seasonal decline, with a slight lower noticed final week. We are able to anticipate an much more important seasonal decline this week.

Though I underestimated the expansion of latest listings knowledge in the course of the peak seasonal weeks by 5,000, it’s encouraging that we noticed development in 2024. Nevertheless, it’s price noting that each 2023 and 2024 will likely be recorded as the 2 lowest years for brand new listings in historical past. The concept that owners would rush to promote their properties in massive numbers is simply fallacious. American owners don’t behave like inventory merchants or get swept up in sensationalist on-line content material of YouTube doomers. They merely go about their regular lives every day.

New listings knowledge for final week:

2024: 51,800

2023: 28,297

2022: 28,471

In a mean yr, about one-third of all properties expertise a worth minimize, which is typical within the housing market. When mortgage charges improve, the share of properties lowering their costs tends to rise. Conversely, this development can decelerate when charges lower and demand will increase, as we lately noticed when charges fell. Nevertheless, mortgage charges have risen once more. We’re on the similar ranges as final yr regardless of having extra stock accessible.

Listed here are the price-cut percentages for final week in comparison with earlier years:

2024: 38.7%

2023: 39percent2022:43%

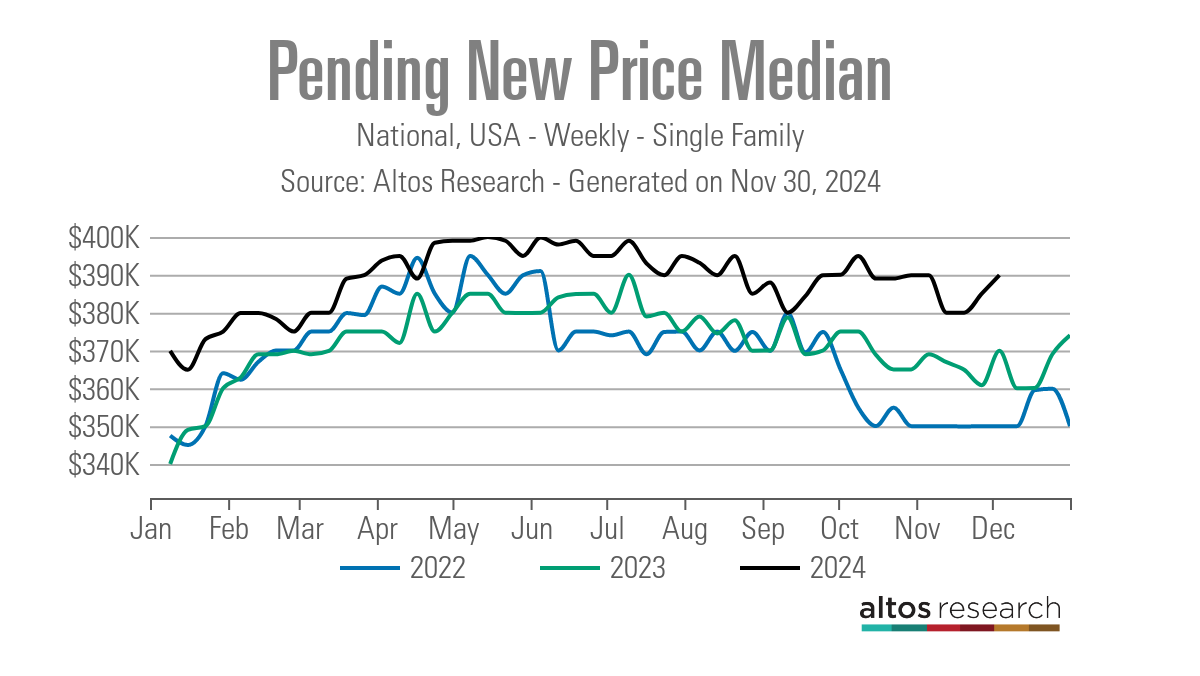

One factor that has stunned me within the 2nd half of 2024 is how resilient our pending new residence worth index has been in a comfortable seasonal interval, with greater stock and mortgage charges above 6%.

The week forward: Jobs week!

There will likely be quite a bit to debate this week — it’s probably the most important week of the month for financial knowledge as a result of it’s jobs week! We’ve got a number of key experiences, together with job openings, the ADP report, jobless claims, and the numerous BLS Jobs report scheduled for Friday. We’ve already noticed a notable drop in yields, so will probably be attention-grabbing to see what occurs subsequent with mortgage charges. We even have ISM knowledge, bond auctions, and a few Fed presidents talking. So buckle up as soon as once more,n and let’s see how the bond market reacts to this week’s knowledge.