What if the story of declining mortgage officer numbers is simply that — a narrative? If you happen to’ve been across the mortgage trade awhile, you’ve certainly heard of a pointy decline in licensed mortgage officer (LOs) numbers. Some reference a 50% drop within the LO inhabitants. Worse but, different imagine that license renewals are down 60%. These numbers — typically offered with pleasure and alarm, relying on the voice — recommend that competitors is scaling down dramatically.

However is that the truth? Lately launched knowledge from intelligence platform RETR, alongside my analysis performed on the NMLS website, tells a really totally different story.

Breaking down the numbers

In line with viral social media put up final month, listed below are the numbers behind mortgage officer decline narrative:

2020: 688,327 licensed LOs

2024: 93,938 licensed LOs

At first look, this paints a dire image. Nonetheless, digging deeper reveals a basic case of evaluating apples to oranges. The 2020 determine displays whole licenses issued — which means an LO licensed in 5 states is counted 5 instances. Conversely, the 2024 quantity counts distinctive people, which means LOs are counted based mostly on particular person standing, as an alternative of what number of licenses they’ve in a number of states.

In line with NMLS knowledge, right here is the actual story behind LO numbers over time (see Determine 1 under):

2019: 165,116 licensed mortgage officers

2022: Peak of 233,938 LOs (a 29% improve from 2019)

2024 Q3: 192,793 LOs (an 18% drop from the 2022 peak)

Whereas there’s undoubtedly been a decline, it’s not fairly as jaw-dropping because the figures floating across the web. Furthermore, RETR’s knowledge on producing LOs — those that’ve really closed a mortgage or two —reveals an analogous pattern: a modest 10% drop, not the 50%-plus some recommend. That’s fairly a distinct story — and one which’s barely much less apocalyptic.

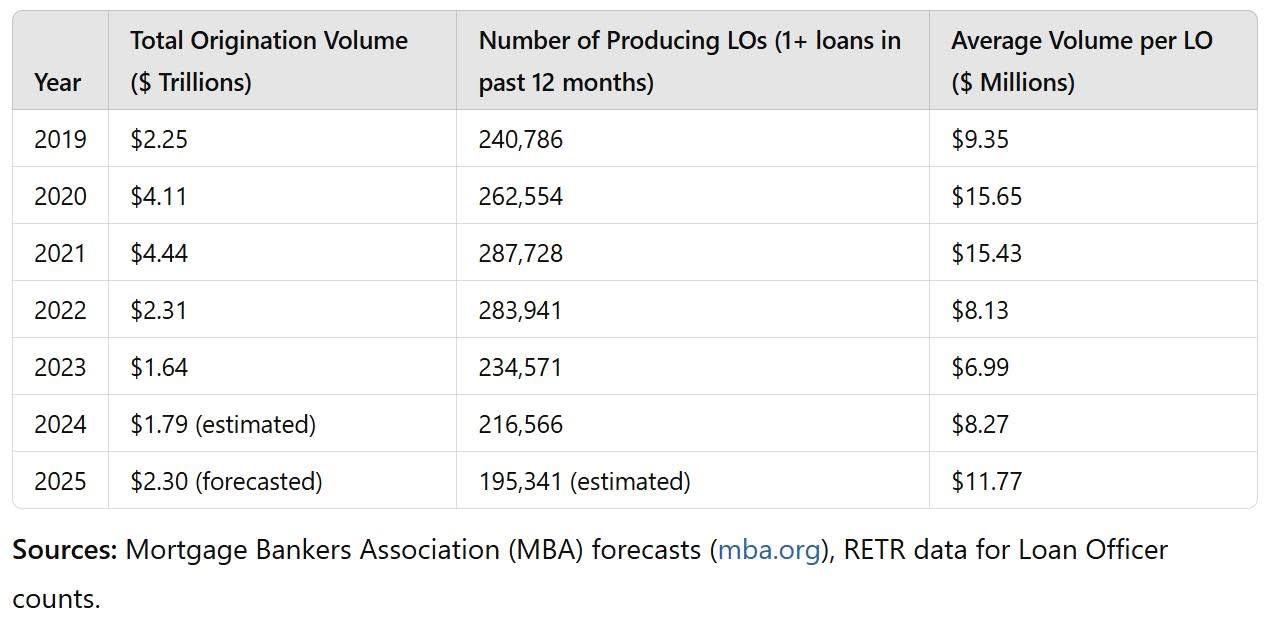

The aggressive panorama tells the larger story

The larger story lies within the aggressive dynamics. Whereas the variety of LOs has declined, common quantity per LO has fallen considerably for the reason that market peak in 2020. In line with knowledge from the Mortgage Bankers Affiliation (MBA) and RETR (see Desk 1 under):

In 2020, common quantity per LO hit $15.65 million.

By 2023, that quantity dropped to $6.99 million — a stark reflection of declining market quantity and better competitors.

What’s the excellent news? Projections for 2025 recommend a 40% improve in common quantity per LO. That will probably be pushed by rising origination quantity and a slight continued decline in producing LOs.

A private reflection to contemplate

For me, these insights had been a wake-up name. I’d allowed the “LO decline” narrative to justify complacency. Nonetheless, the information tells me in any other case. The competitors is fierce, however alternative is plentiful for many who adapt and keep proactive available in the market. Whether or not you imagine that you would be able to or can’t, you’re proper.

The numbers don’t lie. However in addition they don’t inform the entire story. Let this be a reminder: the longer term belongs to those that don’t simply concentrate on surviving, however to those that are centered on innovating and rising all the time.

See you on the high.

Michael McAllister

Founder/President of Empower LO

[email protected]